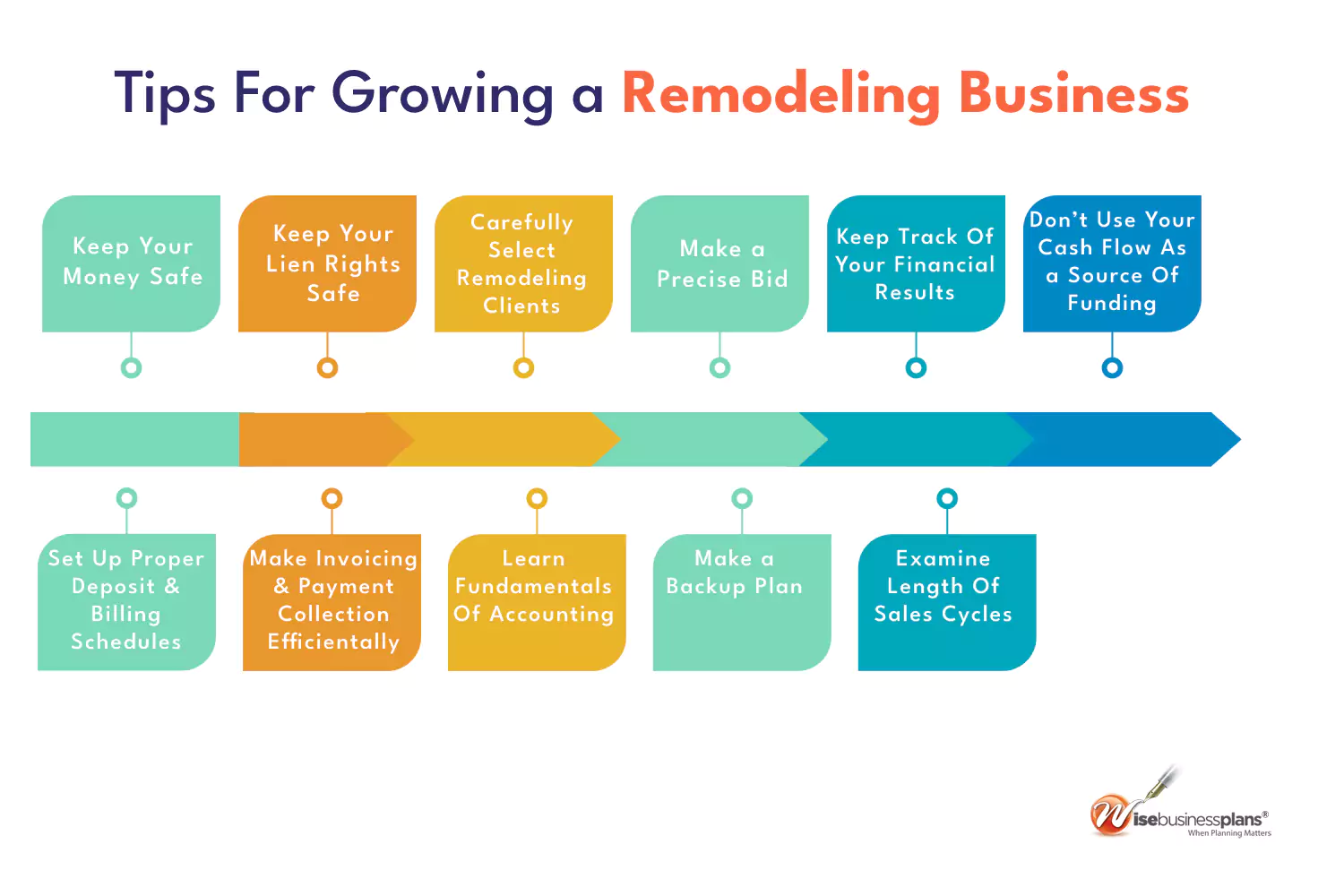

Here are some tips for contractors on how to handle increased demand and expand their remodeling business during a recession.

1. Keep your money safe

There is sometimes a feeling that success is guaranteed when renovation jobs are pouring in the door. However, for a remodeling business, expansion entails a great deal of risk. Your cash outlay for material purchases, labor, and mobilization costs rises as you take on more jobs. While you wait for payments, your business can quickly become underwater.

Cash flow issues are the leading cause of construction company failure, which should come as no surprise. When you’re trying to expand your remodeling business, it’s more important than ever to keep a close eye on your financial statements and look for any gaps in your cash flow forecast.

Are you looking for a simple way to safe your cash reserves? Consider taking out a loan to pay for your materials. Allow someone else to pay for your materials up front while you wait for payment from your customer. Use those funds to pay off other bills that can’t be postponed.

2. Keep your lien rights safe

When a customer delays or defaults on their payment, it becomes more costly the more jobs you have open and the larger they become. That money is necessary to keep your other projects afloat. Your right to file a mechanics lien is the most valuable tool in your payment toolbox, regardless of how much you trust the homeowner to pay.

Remember that when your business is booming, cash flow issues can quickly sink you. Consider filing a mechanics lien to protect your financial assets if a homeowner is delaying payment. A mechanics lien claim can prevent an owner from selling or refinancing their property until you are paid.

3. Carefully select remodeling clients

You can be pickier about the customers you take on when you have more renovation jobs than you can handle. It is critical to select the best clients for your business.

The first step is to ensure that the services you provide meet the expectations of your customers. Is your remodeling company more concerned with project design or construction?

Another important consideration is the location. Consider the distance between your office and the construction site. Working on assignments that are further away can take a lot of time and effort.

It’s also critical to become acquainted with your customers. Make sure they have the specifications nailed down before you start the remodeling process, unless they’re hiring you to design and build a new bathroom. You can see if your personalities mesh well during the interview. This is crucial because you will be working with them for a long time.

4. Make a precise bid

To increase your payment, it may be tempting to overbid. However, it may result in the loss of potential clients. When it comes to remodeling projects, few homeowners choose the first contractor they come across.

It’s critical to evaluate previous projects when determining the bid amount so that your renovation estimate is as accurate as possible. Examine blueprints and bills, for example. You should also factor in all remodeling expenses, including labor, materials, and equipment.

Understanding the return on investment (ROI) of projects is another way to determine the appropriate amount. Bathroom remodels, for example, have a higher return on investment. Research can assist in determining the most accurate renovation cost. Make sure the bid information is well-organized and that the estimated costs are supported by data.

5. Keep track of your financial results

Every homeowner is distinct, and each renovation project is distinct as well. Some jobs will cost more than you anticipated, while others will come in under budget. You can identify trends that you can control by tracking your financial performance over time.

6. Don’t use your cash flow as a source of funding

Remodeling business and business owners frequently use money from personal savings or anticipated cash flow from future jobs to fund current projects. While it is a low-cost method of financing, it requires you to take a significant financial risk in the event of a market downturn or an unexpected drop in business.

If your cash flow is liquid and accessible, it can help your remodeling business survive in the event of a drop in demand. Consider other alternative financing options, such as low-cost merchant cash advances or equipment-based asset financing, instead of using your cash as a financing tool. These options provide you with affordable access to the cash you need to do your job.

7. Set up proper deposit and billing schedules

If a client hires you and then declares bankruptcy or decides not to finish the project, you may be unable to recover the money you’ve spent on materials, labor, equipment, and other supplies without resorting to legal action.

Protect your assets by establishing clear client policies and procedures. Before work can begin, some remodeling business require a deposit of up to 50% of the total job cost. The bill for specific percentages of the total amount due at various points in the project once the job is started.

8. Make invoicing and payment collection more efficient

To save money on hard costs, shorten the time it takes to prepare and send invoices, and simplify the process of sending payment reminders, send invoices electronically. Invoices should include payment policies such as “due upon receipt” or “Net 30 terms“.

Consider accepting credit cards if you don’t already. You may have to pay a small fee for the service, but it could result in invoices being paid much more quickly than they would be otherwise.

9. Learn the fundamentals of accounting

Percentage of completion accounting, according to remodeling business accounting experts, is critical for all remodeling business owners to use and monitor because it has a direct impact on cash flow.

Invest in software that makes this figure simple to calculate (to arrive at the percentage complete for each job, divide costs to date by total estimated costs). Monitor the percentages for all of your jobs on a regular basis so you don’t get caught off guard when a job’s timeline or budget shifts.

10. Make a backup plan

Develop four to six weeks of rolling cash flow projections at the very least, so you have a real-time picture of your company’s financial situation. Aim to have six months’ worth of cash flow reserves (based on your operating expenses) in a liquid, interest-bearing deposit account that you can access in the event of an emergency.

11. Examine the length of your sales cycles

While larger remodeling projects may require more time and resources to quote, complete, bill, and collect payment, smaller jobs may require far less time and resources to quote, complete, bill, and collect payment. Keep track of your company’s timelines for converting job quotes into live projects. Weekly review your project schedules to see if seasonality, demand, or economic trends require you to diversify your workload in order to maintain optimal cash flow.

Cash flow management is a difficult aspect of owning a remodeling company, but it isn’t one that requires you to be reactive. Implement these best practices to create a financially stable and thriving remodeling company.

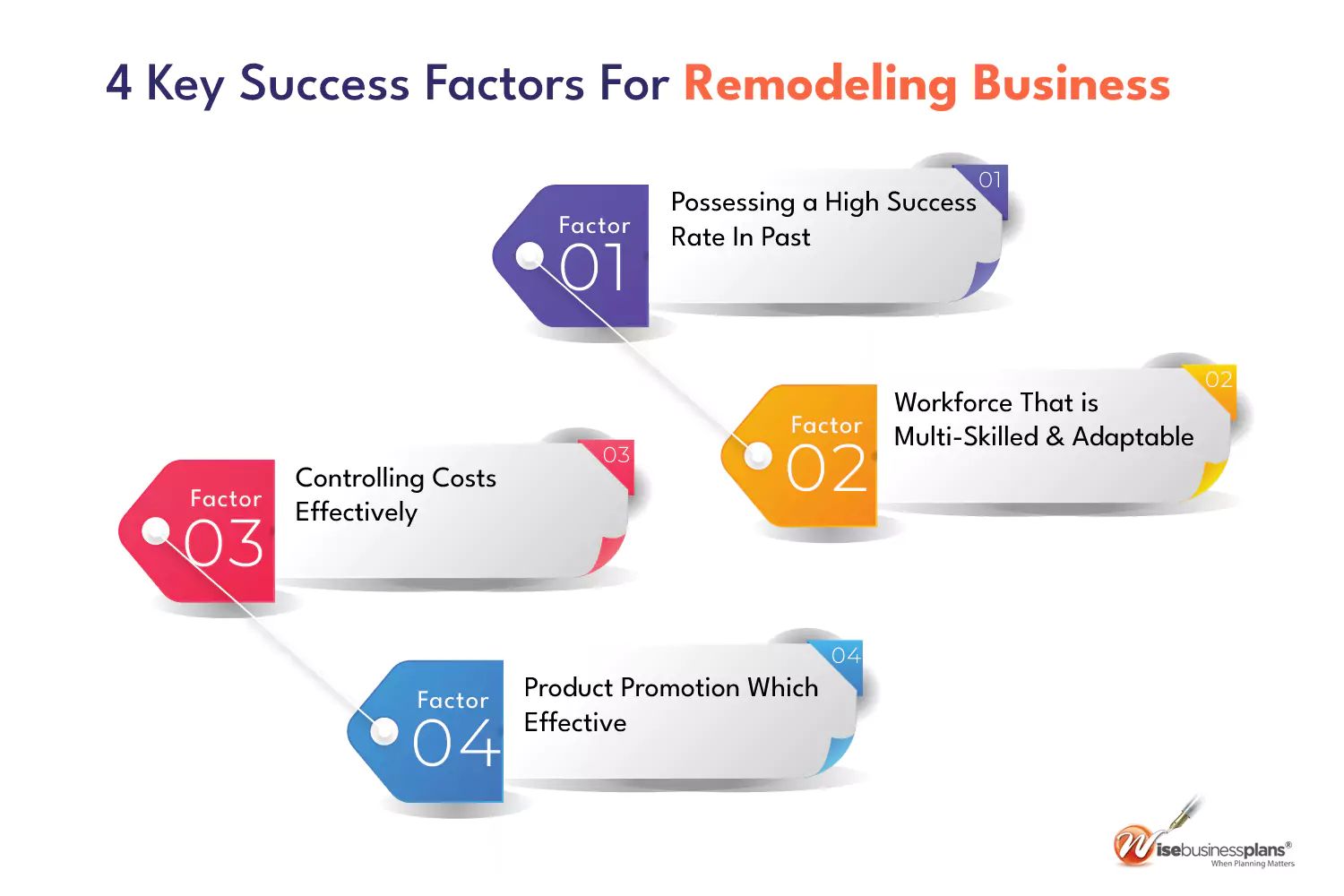

- Possessing a high success rate in the past (including completed prior contracts): Companies with a strong reputation for having the financial, managerial, and technical capacity for remodeling projects attract potential clients. Successful remodeling companies can show a portfolio of previous work and testimonials from happy clients.

- Workforce that is multi-skilled and adaptable: Reputable tradespeople and subcontractors are available on a project-by-project basis for successful remodeling companies.

- Controlling costs effectively: Successful remodeling businesses maintain tight cost controls and have access to low-cost input materials to maintain competitive pricing.

- Product promotion which effective: To generate publicity and new contracts, successful remodeling companies have a strong marketing department.