- Company

- Business Plan

- Sample Business Plans

- Steps & Timeline

- Work at a Glance

- Market Research at a Glance

- Overview

- Investor Business Plan

- Bank Business Plan

- Strategic Business Plan

- Nonprofit Business Plan

- Franchise Business Plan | Business plan template ppt

- L-1 Business Plan

- E-2 Business Plan

- EB-5 Business Plan

- EB-5 Regional Centers

- Merge and Acquisition Business Plan (M&A)

- Private Placement Memorandums (PPM)

- Professional Feasibility Study

- PowerPoint Presentations

- Pitch Deck Presentation Services

- Market Research

- Plan

- Build

- Fund

- Shop

- Contact Us

- Talk to Us 1-800-496-1056

Bookstore Business Plan Template

Getting your own bookstore off the ground requires a business plan. Here is a bookstore business plan template that includes the important elements you need to include in your business plan.

Fill the Form to Download Business Plan Templates

To ensure your bookstore business success in this highly competitive market, you need a properly structured bookstore business plan. With over 12 years of experience, we have helped over 5,000 entrepreneurs create business plans to start and grow their bookstore businesses. Using the following bookstore business template, you can put together an effective business plan for art gallery.

Things to Know Before Writing a Bookstore Business Plan

A wide variety of books, newspapers, and periodicals is primarily sold by companies in this industry, including trade books, textbooks, magazines, paperbacks, and religious books.

Manufacturers and wholesalers purchase these products, both domestically and internationally. Operators then sell these goods to consumers in retail stores.

Having enjoyed strong gains in the second half of the year, bookstore sales increased 39% over 2020, according to preliminary estimates from the U.S. Census Bureau.

The company posted sales of $9.03 billion, compared to $6.50 billion in the pandemic-ravaged year of 2020.

The major products and services offered by this industry are

- Trade books

- Religious goods (including books)

- Textbooks

- Magazines and newspapers

- Other merchandise

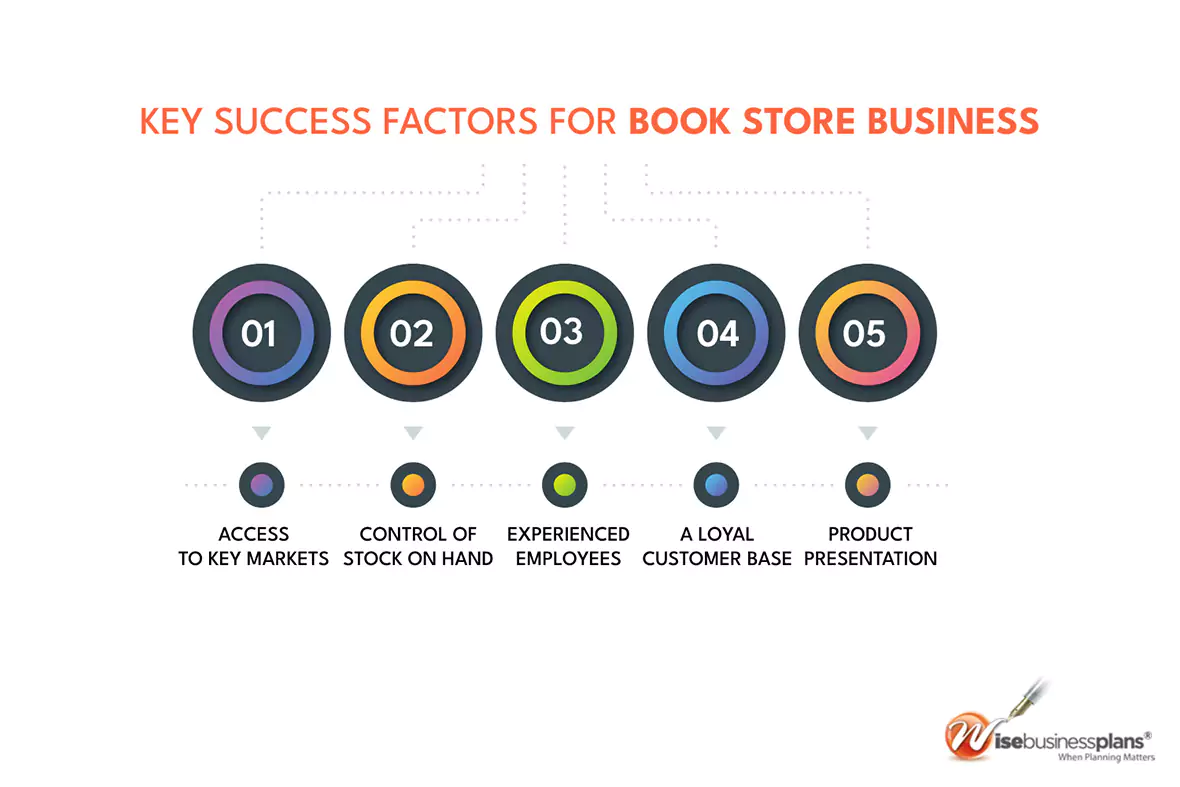

Key Success Factors for the Book Store Business

Despite the challenges of the Book Store industry, we have identified 5 factors that can help you boost profitability, efficiency, and ultimately success.

- Access to key markets: By being located near key markets, operators can maximize exposure to consumers.

- Control of stock on hand: Operators must ensure top-selling items are always available, especially during peak times (e.g. the winter holiday season and graduation season).

- Experienced employees: Operators must have employees who have relevant knowledge of the products currently being sold to satisfy customers.

- A loyal customer base: Operators can reward their loyal customers with promotional discounts, superior customer service, and author signings.

- Attractive product presentation: Stores need to present their products in an inviting manner to encourage impulse purchases.

Free: Business Plan Examples

Do you need help creating a business plan? Check out these six free, proven business plan examples from different industries to help you write your own.

What is a Bookstore Business Plan?

A business plan for a bookstore is a written document that sets your company’s financial goals and discusses how you’ll reach them.

A solid, comprehensive strategy will serve as a road map for the next three to five years of the bookstore business. Any bank or investor you approach will require a bookstore business plan, so putting one together will be critical to securing funding.

In short, writing a business plan can help you succeed if you’re thinking of starting a bookstore business or pitching to investors or venture capitalists.

Why You Need a Bookstore Business Plan

If you want to start a bookstore business or expand an existing one, the first thing you need to do is to write a business plan. A business plan is also necessary for attracting investors who want to know if your bookstore is on the right track and worth investing in.

A solid, detailed plan gives you a clear path to follow, forces you to examine the viability of a bookstore business idea, and may help you better understand your company’s finances and competition.

Bookstore owners who have a business plan grow 33% faster than those who don’t, and 72% of fast-growing businesses have one.

A bookstore business plan is a living document that should be updated annually as your company grows and changes.

How Much Does it Cost to Open a Bookstore?

The cost of opening a bookstore varies depending on the location and size. The cost of leasing retail space varies based on the location. A typical initial opening cost for a bookstore is about $22,000 USD, and this does not include rent or utilities for the first month.

Funding Sources for Bookstore Businesses

Asking family and friends to invest in your bookstore is a great way to start. Once you’ve set a budget and identified what you’ll need to start the store, take the services of your friends and family to help you get it off the ground. You might need to present the willing ones a solid business plan to reassure them that their chances of making a profit are good.

Bank loans and angel investors are the two most common sources of funding for a bookstore. When it comes to bank loans, banks will want to look over your bookstore business plan to make sure you’ll be able to pay it back with interest.

The loan officer will not simply want to ensure that your financials are reasonable in order to gain this confidence. They will, however, expect to see a professional plan. They will be more confident in your ability to run a business successfully and professionally if you have a plan like this.

Angel investors are the second most popular source of finance for a bookstore business. Wealthy individuals who will write you a check are known as angel investors.They will either want equity in exchange for their capital or will let you have a loan, similar to a bank.

Looking to Build Business Credit for Your Bookstore?

Build your business credit quickly with an easy approval net 30 account from Wise Business Plans. Or check out the top 10 net 30 vendors to find the best one for you to help build your business credit.

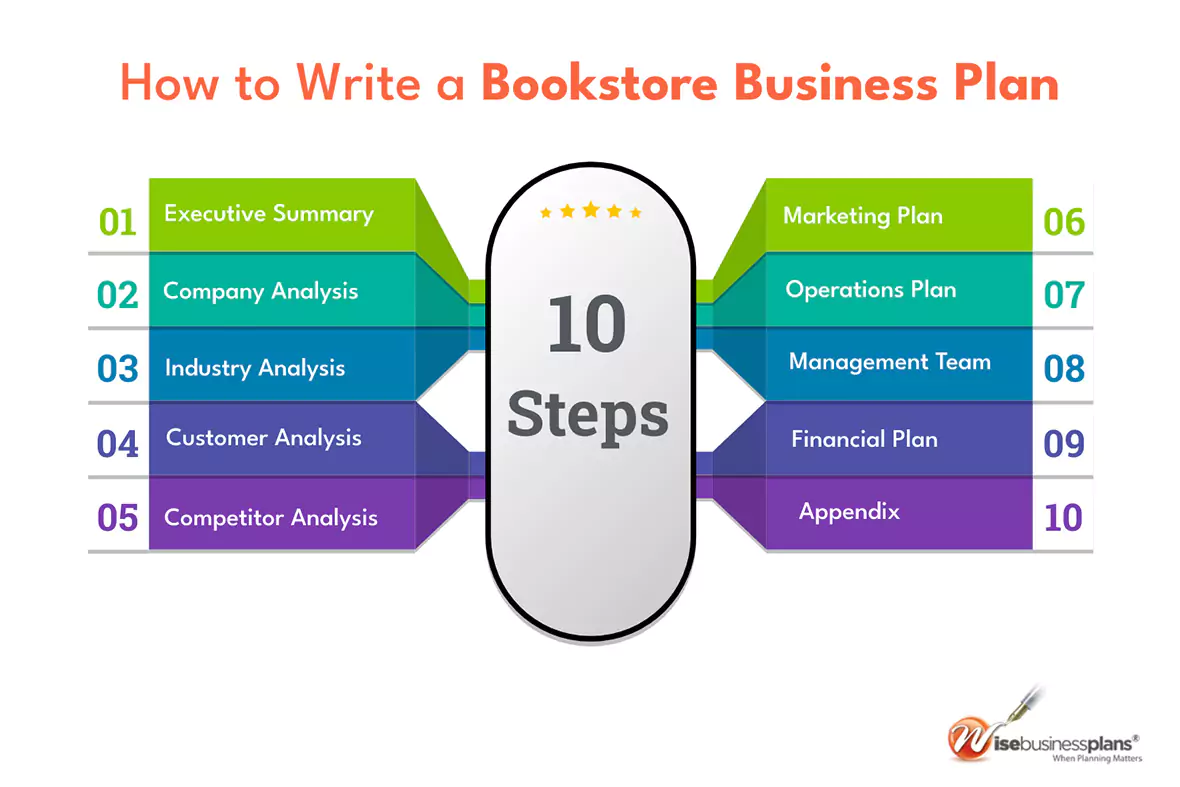

How to Write a Bookstore Business Plan

To write a bookstore business plan, you don’t need to be an expert. Our step-by-step guide will show you how to write a bookstore business plan, or you can just download our proven sample business plan pdf to get a better idea.

Executive Summary

The executive summary is the most important part of the document since it outlines the whole business plan. Despite the fact that it appears first in the plan, write the executive summary last so you may condense key concepts from the other nine parts.

It’s a part that catches the investor’s eye and provides key information about your company’s overview and upcoming short- and long-term goals.

Tell them what kind of bookstore you have and what stage you’re in; for example, are you a startup, do you have a bookstore that you want to expand, or do you have a lot of bookstores?

Finally, an executive summary should provide investors with a preview of what they may expect from the rest of your document.

- Provide a high-level overview of the bookstore industry

- The name, location, and mission of your bookstore

- A description of your bookstore business, including management, advisors, and a brief history

- Discuss the type of bookstore you are operating, Give an overview of your target customers., and how your product differs from competitors in the industry

- Create a marketing plan that describes your company’s marketing strategies, sales, and partnership plans.

- And give an overview of your financial plan

Check out these executive summary examples to help you write a perfect one for your business plan.

Free: Executive Summary Examples

An executive summary is the most important part of your business plan, and it need not be challenging to write. This is why we have put together some awesome free Executive Summary examples for you.

Company Analysis

The company analysis follows the executive summary as the second section of a business plan. Your company overview will be short and clear, similar to the executive summary.

Even if they just have a few minutes, your reader has to understand what your company does and who your customers are.

The following sections will be included in your business plan’s Company Analysis:

- Company summary: Your company analysis will describe the type of bookstore you are operating and its future goals. The type of bookstore you might be focused on are: Religious bookstore, Traditional bookstore, Used bookstore, Specialty bookstore(new age, comic and story books, fiction books), etc.)

- Company history: When and why did you start your bookstore?

- Management team: Who runs the company, and other key positions.

- What milestones have you achieved so far? Your milestones could include sales goals achieved, new store openings, etc.

- Legal structure and ownership: Your reader will want to know what business entity your company is: a sole proprietorship, LLC, partnership, or corporation.

- Locations and facilities: Information about your workspaces or plans to acquire them.

- Mission statement: An overview of your company’s guiding principles. Learn how to write a perfect mission statement.

Industry Analysis

You need to include an overview of the bookstore in the industry analysis you performed before sitting down to write your bookstore business plan.

While this research may appear to be unnecessary, it helps you to build strategies that maximize business opportunities while lowering or avoiding the identified risk.

You may learn a lot about the bookstore industry by doing research. It helps you in understanding the market wherein you operate.

The third purpose for conducting market research is to demonstrate to readers that you are an industry expert.

Industry analysis can be presented as a 8-step process when written as part of a company’s business plan.

- Give a quick overview of the bookstore industry. Define the bookstore business in terms of size (in dollars), historical background, service region, and products.

- Examine previous trends and growth patterns in the bookstore industry.

- Identify the market’s major competitors.

- Age, gender, and general lifestyle of the targeted market

- Who are the market’s main suppliers?

- Determine the factors that have an impact on the bookstore industry. These might include government regulatory rules and other businesses’ competitive activities.

- Using research data, the industry forecast expected growth. Predictions should be made for both the long and short term.

- Describe how your bookstore business intends to position itself in the industry. Concentrate on how your bookstore business can benefit from opportunities highlighted in the industry.

Customer Analysis

The customer analysis section is an important part of any bookstore business plan since it evaluates the consumer segments that your company serves. It identifies target customers, determines what those customers want, and then explains how the product will meet those requirements.

Here are some examples of customer segments: students, children, techies, teens, reading fans, old aged persons, etc.

Customer analysis may be divided into two parts: Psycho-social profiles (why your books suits a customer’s lifestyle) and Demographic profiles (descriptions of a customer’s demographic qualities).

In terms of demographics, you should include information on the ages, genders, locations, and income levels of the consumers you want to serve. Because most bookstores serve consumers who live in the same city or town, such demographic data is easily accessible on government websites.

The psychological profiles of your target clients reveal their wants and needs. The better you understand and identify these demands, the better your chances of attracting and retaining customers will be.

Competitor Analysis

It is necessary to do a competitor analysis. Not least because you may use their data to define your goals, marketing plans, tactics, new product lines, pricing, and more. Use competitor analysis to:

- Identify the strength and weaknesses of your bookstore competitors.

- Search for opportunities to distinguish your bookstore from competitors.

- Set your product’s price.

On the market, you will almost certainly discover some extremely powerful competitors, some of whom will be offering things similar to yours at unbelievably low costs. However, not every competitor works with low-cost, low-quality books

The first step is to determine who your direct and indirect rivals are.

The direct competitors consists of other bookstore businesses that offer essentially the same products to the same people as you do.

Indirect competitors consists of brands that offer somewhat different things but can meet the same customer demands, You will likely have online competitors who sell similar items to you. Libraries and eBooks are also included as indirect competitors.

Once you’ve identified the competitors, concentrate on the direct, head-to-head competitors, since they are the most threatening to your bookstore business — but keep an eye on the indirect competitors as well, just in case.

Provide an overview of each direct competitor’s business and detail their strengths and weaknesses.

You will be able to position yourself competitively in the market if you perform proper competitors research. Perform a SWOT Analysis to learn your competitors’ strengths, weaknesses, and competitive advantages in the following areas:

- Prices – Are they cheaper or more costly than you and other bookstores, what value do buyers get for that price, and does shipping significantly raise the price?

- Quality – The quality books they provide, the perceived worth in the eyes of the customers

- Customer service – How they respond to their consumers, whether they treat them poorly or well, and the degrees of satisfaction customers show

- Reputation — The sum of everything mentioned above: their credibility, how loved the brand is, and the loyalty of their customers

The final section of your competitive analysis should include a list of your areas of competitive advantage. for example: Are you going to offer premium books? Will you offer unique books that your competitors don’t offer? Will you offer better pricing or will you offer greater customer support?

Consider how you will outperform your competitors and include them in this portion of your bookstore plan.

Free: SWOT Analysis Examples

Take advantage of our free SWOT analysis examples. Make your business future-proof by identifying your strengths, weaknesses, opportunities, and threats using this free SWOT Analysis Template.

Marketing Plan

Creating a marketing plan for a bookstore business involves identifying the target demographic and finding products that suit their preferences. Bookstore owners need to constantly seek out books that their competitors do not carry.

As part of your marketing plan for a bookstore, you should include:

Pricing and Product Strategy

Your bookstore business must offer books that are unique, likable in public, and different from those of your competitors. Research what your competitors carry and how they price their products. A unique bookstore collection identifies your store as the place to go for unique books and differentiates it from others.

Placing and Promotions

Place refers to the location of your bookstore. Is your bookstore business near an school, college, university building or town that has a high population? If you plan to target a specific geographic region, mention how your location will impact your success.

Promoting your bookstore is the final part of your marketing plan. In this step, you document how you will drive customers to purchase your bookstore. A few marketing methods you could consider are:

- Marketing in local newspapers and magazines

- Approaching bloggers and websites

- Event Marketing

- Marketing on social media

- Pay Per Click marketing

- Adding extra appeal to your storefront to attract passing customers

- Ongoing Customer Communications

Operations Plan

While the previous sections of your bookstore business plan described your goals, your operations plan discusses how you will achieve them.

An operations plan is helpful for investors, but it’s also helpful for you and employees because it pushes you to think about tactics and deadlines.

Your operations plan should be divided into two individual parts, as seen below.

All the daily tasks involved in running your bookstore business, such as serving customers, ordering inventory, maintaining a clean store, etc., are short-term processes.

Long-term goals are milestones that you aim to reach. These may include the dates when finalizing the lease agreement for the storefront bookstore or Reach break-evens. It might also be when you plan to launch a new bookstore or to serve 1000th customer.

Management Team

When writing a bookstore business plan, the management section’ outlines your management team, staff, resources, and how your business ownership is structured.

A strong management team is necessary to demonstrate your bookstore’s ability to succeed as a business. Highlight the backgrounds of your key players, emphasizing the skills and experiences that demonstrate their ability to grow a business.

You and/or your team members should ideally have prior experience working in a bookstore. If so, emphasize your knowledge and experience. However, you should emphasize any experience that you believe will help your bookstore business succeed.

Consider forming an advisory board if your team is lacking. An advisory board would consist of 2 to 8 people who would act as mentors to your company. They would assist in answering questions and providing strategic direction. If necessary, seek out advisory board members with experience running bookstore and/or retail and small businesses.

Financial Plan

As part of your financial plan, you should present a 5-year financial statement broken down monthly or quarterly for the first year, and then annually. Business financial statements include your income statement, balance sheet, and cash flow statement.

Income Statement

A profit and loss statement is more commonly called an income statement. It shows your revenue and subtracts your expenses to determine whether you were profitable or not.

As you develop your income statement, you need to develop assumptions. For example, will you serve 20 clients per day or 50? Will sales increase by 3% or 15% per year? As you can imagine, your assumptions have a significant impact on your financial forecast. Do your best to verify your assumptions by conducting research.

Free: Income Statement Template

Create a financial statement for your business by downloading our free income statement templates.

Balance Sheet

While balance sheets include much information, to simplify them to the key items you need to know about, balance sheets show your assets and liabilities.

The balance sheet shows your bookstore’s net value at a specific point in time. It categorizes all of your company’s financial data into three categories:

- Assets: Tangible goods with the monetary worth that the company owns.

- Liabilities: Debt owing to a company’s creditor.

- Equity: The net difference when the total liabilities are subtracted from the total assets.

The equation that expresses the relationship between these financial data elements is Assets = Liabilities + Equity.

Create a pro forma balance sheet for your bookstore business plan that highlights the information in the income statement and cash flow projections. A balance sheet is normally prepared once a year by a company.

Balance sheets indicate your assets and liabilities, and while they contain a lot of information, they are simplified to highlight the most important things you need to know.

For example, spending $150,000 to build out your bookstore business will not result in instant revenues. Rather, it is an asset that should help you earn money for many years to come.

Similarly, if a bank sends you a check for $700,000, you do not have to pay it back right now. Rather, that is a liability that you will repay over time.

Free: Balance Sheet Template

Create a financial statement for your business by downloading our free balance sheet templates.

Appendix

List any additional material you cannot include elsewhere, such as resumes from key employees, licenses, equipment leases, permits, patents, receipts, bank statements, contracts, and personal and business credit histories.

Attach your full financial projections along with any supporting documents that make your plan more compelling in the appendix. You may, for instance, include some of your apparel designs.

Bonus Tip: Learn how to write a business plan appendix for your bookstore business.

Summary of the Bookstore Business Plan

A bookstore business plan is a worthwhile investment. As long as you follow the template above, you will become an expert in no time. By following the template, you will understandable the bookstore business, your competitors, and your customers. The plan will help you understand the steps necessary to launch and grow your bookstore.

Do you want to Finish Your Bookstore Business Plan in less the one day?

Wouldn’t it be nice if your business plan could be completed faster and easier?

With wise business plans Business Plan Template, you can finish your plan in just 6 hours or less with a 30-Day Money-Back Guarantee!

In addition, you can download our 300+ free business plan templates covering a range of industries.

OR, we can develop your bookstore business plan for you

Since 2010, Wise business plans’ MBA professional business plan writers has developed business plans for thousands of companies that have experienced tremendous success.

Download Our Bookstore Business Plan Template

We will show you some real-world business plan examples so you may know how to write your own, especially if you are seeking a bank loan or an outside investment and need to use SBA-approved formatting.

Get in Touch

Contact Us Today For A Free Consultation

- Business Planning

- Bank Business Plan

- Investor Business Plans

- Franchise Business Plan

- Cannabis Business Plan

- Strategic Business Plan

- M&A Business Plan

- Private Placement

- Feasibility Study

- Pitch Deck

- Pitch Deck

- Market Research

- Sample Business Plans

- Hire a Business Plan Writer

- Business Plan Printing

- Business Valuation Calculator

- Business Plan Examples

- Real Estate Business Plan

- Business Plan Template

- Business Plan Pricing Guide

- Nonprofit Business Plan

- Business Plan Makeover

- Business Funding

- Business E-learning Series

- Business Assets

- 1-800-496-1056

- (613) 800-0227

- +44 (1549) 409190

- +61 (2) 72510077

© Wise Business Plans®. All rights reserved.