Businesses buy, sell, borrow and lend, and their financial credibility is shown with a business credit score.

A business credit score determines its creditworthiness. Credit agencies, suppliers, lenders, and vendors see your business credit score to decide business terms with you.

We have discussed business credit scores in this article. It will help you understand what a business credit score is, why should you care for it, and how you can get and improve your business’s credit score.

Want to write a business plan?

Get help from our business plan expert now!

What is a business credit score?

A business credit score is your business’s creditworthiness. It shows if your business makes bills and loan payments on time and keeps its financial promises.

There are many variables counted in calculating the business credit score. Some of the variables are:

- payment history,

- age of credit history

- debt and debt usage

- industry risk

- company size

What is a business credit report?

A business credit report is prepared by the credit agencies. It discusses all the factors that affect your business credit score, shows implications, and suggests how you can improve the weak variables.

The top business credit agencies are Dun & Bradstreet, Experian, FICO, and Equifax.

A business credit report includes:

- Business’s financial profile

- Business Tradeline history

- recent credit inquiries

- legal filings, including judgments, collections, & bankruptcies.

All of the business credit agencies offer business credit reports at a fee. Some lenders send the trade credit information to the reporting credit unions voluntarily.

Some information may be missing from your business credit report if your lender is not sharing the information with the reporting agency. Keep checking your business credit score regularly.

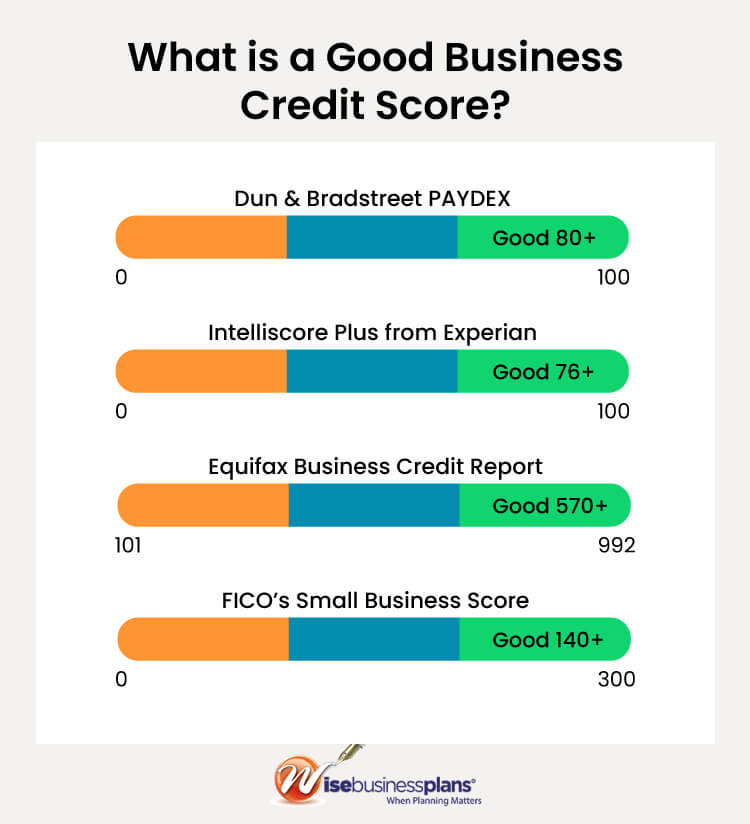

What is a good business credit score?

Simply put, a higher score on a credit agency business credit scale is a good credit score.

The number or point where we may call a business credit score a good score depends on the specific credit reporting agency. As a rule of thumb, a higher score is a better score.

For example, the Dun & Bradstreet PAYDEX score, which is the go-to business credit score, gives a score in the range of 1-100. The higher the score is, the better.

Here are the business credit score ranges for different credit reporting agencies.

- Dun & Bradstreet, 1-100

- Experian, 1-100

- Equifax Business Credit Risk Score, 101-992

- Equifax Business Failure Score, 1000-1610

- FICO SBSS Credit Score, 0-300

The different ranges of credit scores show different variables used in calculating each score.

What is a good business credit score?

How Is A Business Credit Score Calculated?

All credit reporting agencies use different criteria to calculate your business credit score. One thing that counts the most is your payment history, or when you pay your bills.

The industry standard business credit score is the Dun & Bradstreet PAYDEX score which calculates your business credit score on only one factor. They see if you pay your business bill before time, on time, or after the due date.

For example, if your Dun & Bradstreet PAYDEX score is 80 or more, it means you pay bills 30 days before the due date.

Note that your business credit score will be different with each credit reporting agency. This is because each agency uses different criteria and variables to calculate the score.

A contrast to the example of Dun & Bradstreet PAYDEX score is Experian Intelliscore Plus which uses over 800 variables to calculate a business credit score.

These are the top variables that Experian Intelliscore Plus uses.

- Outstanding debts

- The debt you have, relative to credit available

- Borrowing frequency

- Your company size

- Years in business

How to Check Business Credit Score?

As business credit scores are different from personal credit scores in almost every way, the process of checking a business credit score is also different.

Sometimes, you may have to pay for checking your business credit score.

Here is how you can check your business credit score with Dun & Bradstreet, Experian, and Equifax.

Dun & Bradstreet PAYDEX Score

Dun & Bradstreet offers free business credit score checking and monitoring. You can sign up with the Dun & Bradstreet Credit Signal program.

Dun & Bradstreet offers four business credit scores. You can see these scores and monitor changes with the Bradstreet CreditSignal program. It lets you see credit scores and ratings for a 14-days period.

Equifax

Equifax offers paid business credit score reporting. You can order the business credit score for one business for $99.95.

They offer group discounts. If you buy business credit score reports for five businesses, you’ll pay $399.95. See more about their pricing on the Equifax website.

Experian Intelliscore Plus

Experian offers business credit reports at a cost. You can get a one-time business credit report for $39.95.

You can also order the annual subscription for $189 per year. This plan lets you monitor your business credit score report. Know more about Experian Intelliscore Plus.

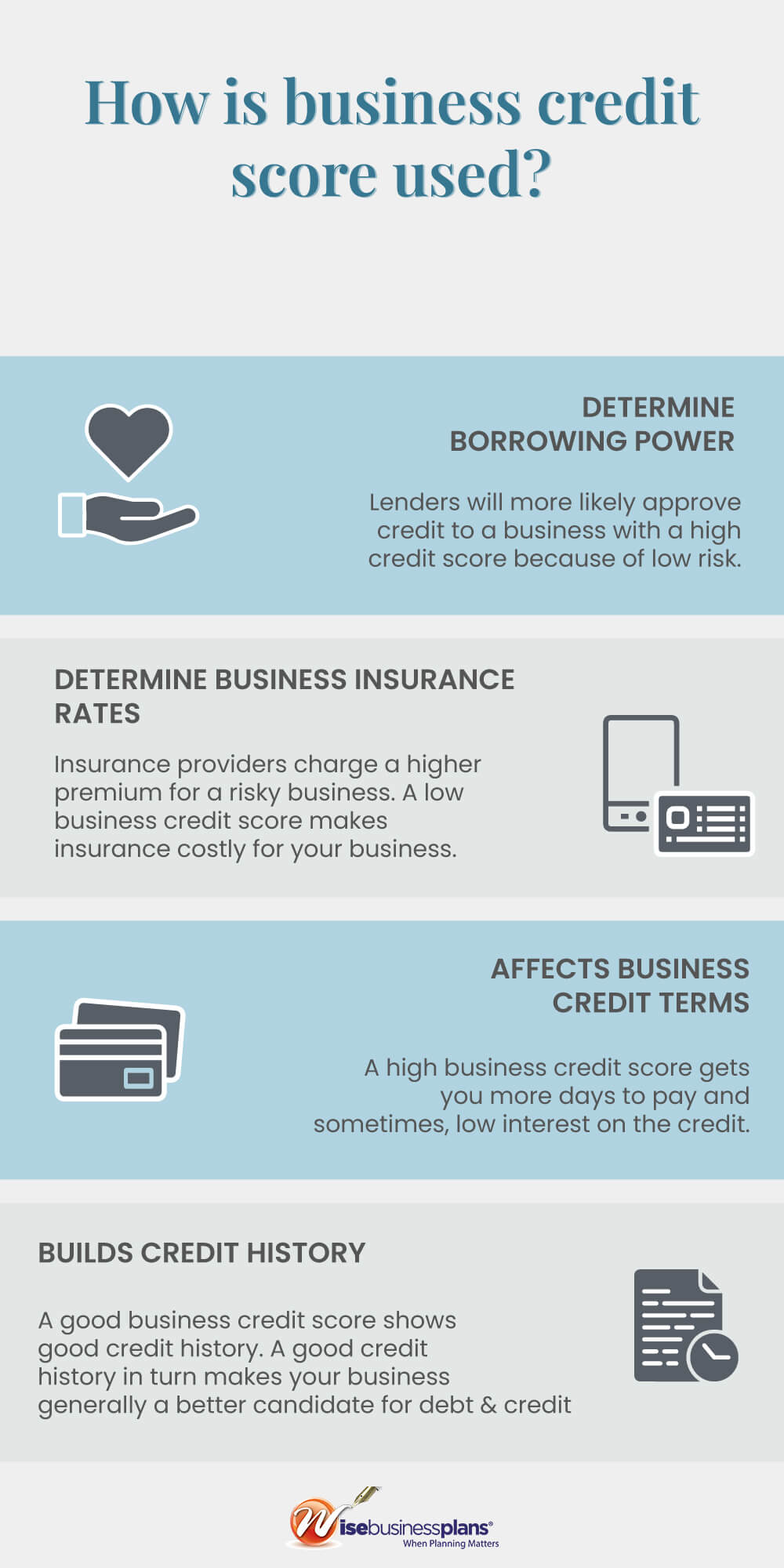

How are Business Credit Scores Used?

Business credit scores represent your business’s creditworthiness.

The lenders and suppliers will look at your business credit report to determine the business terms with you.

A business credit score is used in three major ways.

Determine your borrowing power

A good credit score means your borrowing options are better. You can get a bigger credit line at cheaper rates with a good credit score.

Similarly, a bad credit score can limit your credit options. Your credit line may be smaller and you might have to pay higher interest on the loan.

Though good business credit is not the only factor in deciding your credit for your business, it is one of the most important.

Get more time to pay

A good business credit score shows that you pay your bills on time. Your lenders and suppliers feel comfortable doing business with you. This in turn gets you more time to pay your bills and debts.

Determine your rate for business insurance

The business insurance price directly depends on your business performance. If the credit history of your business is good, you’ll pay a lower insurance premium. You’ll pay higher insurance premiums with a bad business credit score.

What is the Cost of Small Business Insurance?

Read our guide about small business insurance costs.

OR

Take the leap & get a free small business insurance quote. Call 1-800-496-1056 to receive a free quote

Access our free business plan examples now!

How is a personal credit score different from a business credit score?

A personal credit score is different from a business credit score in terms of the credit reporting agencies, credit score range, access, and data.

The top credit reporting agencies are Dun & Bradstreet, Experian, Equifax, and FICO. Dun & Bradstreet only offers business credit reporting and scores.

The personal credit score range is 300-850. However, the business credit score range is different with each credit reporting agency.

Some lenders will only look at your business credit score but that’s mostly at the lender’s discretion. In the case of small businesses, some lenders may also consider your personal credit score.

Why you should check your business credit score?

Many small business owners don’t know about their business credit score. Here are a few reasons why you should check your business credit score regularly.

Stay Sharp. Business credit scores may mix. The credit reporting agencies may miss any bills or your lenders or vendors may not report some transactions which can lower your business credit score.

Monitor changes. When new information is reported to a credit reporting agency, your business credit score changes. Keep checking to know if the new information is factual and if there is anything misstated.

Prevent fraud. Identity theft and fraud are getting common. Monitor your business credit report to spot any suspicious activity.

Increase chances for credit. When you understand your business credit score and how you can improve it, your chances of securing a credit line for your business are higher.

How to Start and Build your business credit score?

Building your business credit is not hard. Your financial discipline forms the basis of a good business credit score.

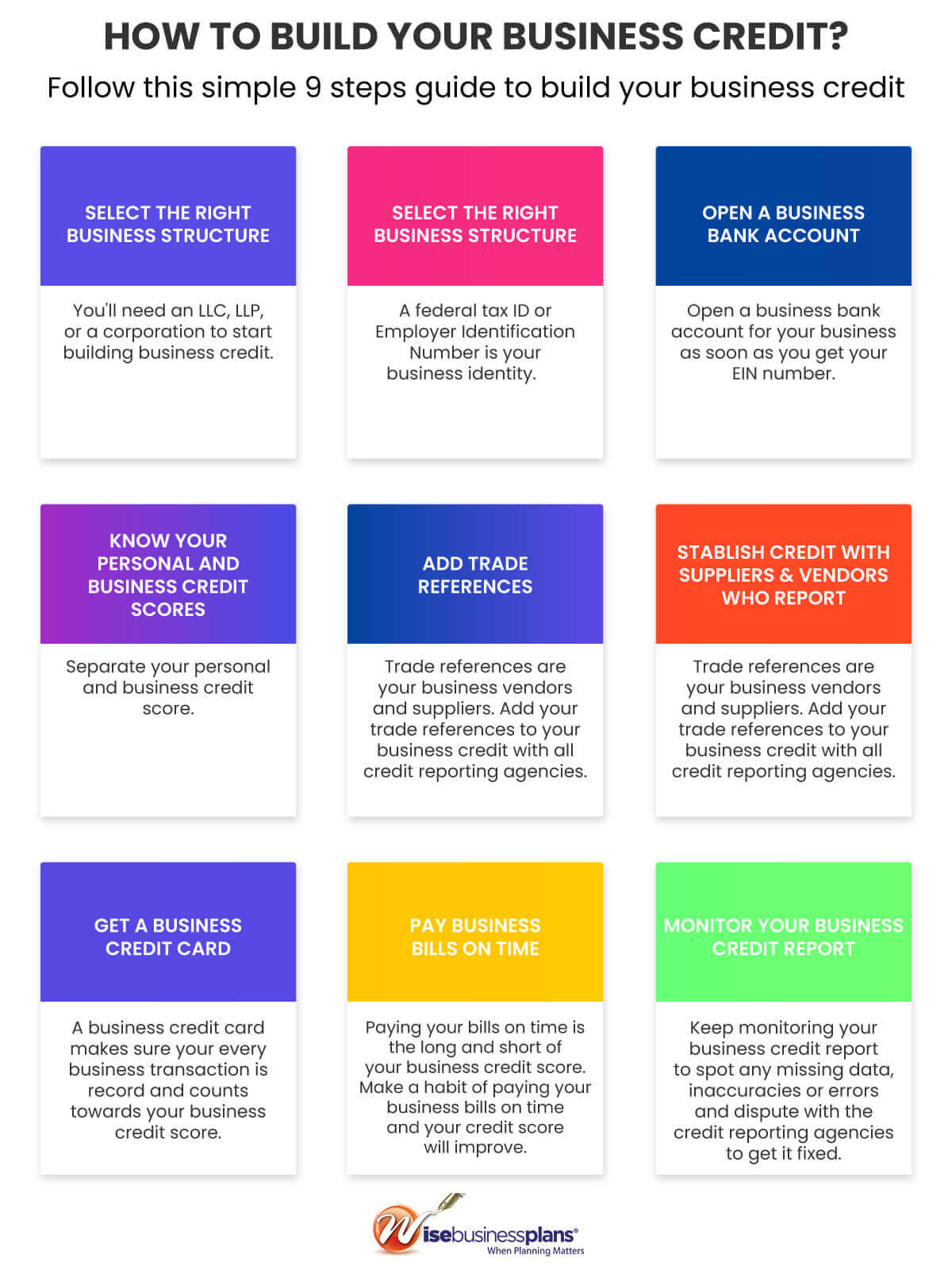

Follow these 9 simple steps to establish and build your business credit score.

1- Select the Right Business Structure

You need a business entity by forming an LLC, LLP, or Corporation as the sole proprietorship does not create a distinct legal entity.

Get help from your legal advisor on the best legal structure for your business.

2- Get an EIN (Employer Identification Number)

Apply for a Federal Tax ID with IRS (also called EIN). Your EIN identifies your business. You need the EIN for filing business tax returns, opening a business bank account, and applying for business licenses & business credit cards.

3- Open a Business Bank Account

Your business bank account separates your personal expenses and business expenses.

Once you have an EIN, you can apply for a business bank account and start building your business credit score.

Your business bank account works as a reference for your credit applications and provides important data for your funding application.

See our list of the best business bank accounts and open a bank account for your business.

4- Know your Personal and Business Credit Scores

You are entitled to one personal credit report every 12 months by federal law. Go to AnnualCreditReports.com and request a personal credit score. Check for any inaccuracies or errors and report them to the credit reporting agencies.

Next, check your business credit score. If you are a new business or you don’t have a business credit score yet, register for a D-U-N-S number with Dun & Bradstreet.

Knowing your personal and business credit scores will help you establish both credit scores separately and deepen your understanding of the credit scores.

5- Add Trade References

Adding your trade references to your business credit history helps you build your business credit.

Your suppliers and vendors are not required to share information with the credit reporting agencies, you can do that on your own.

Your business’s trade experiences, payment pattern, outstanding bills & debts, years in business, and size of the business are some of the top factors contributing to your business credit score.

6- Establish Credit with Suppliers & Vendors who Report

Not all suppliers and vendors report to the credit reporting agencies. This missing data negatively impacts your business credit score.

You are paying your bills on time but still, the business credit score does not improve because of the non-reporting. Working with the suppliers and vendors who report to the credit bureaus will solve the problem.

Check this list of Net-30 Vendors for your Business and start building your business credit.

Need to Build Business Credit Fast?

Start building your business credit score with a Net-30 account from WiseBusinessPlans.

We offer quick application processing without a personal credit check.

7- Get a Business Credit Card

A business credit card helps you build business credit.

Get at least one business credit card in your business name. Keep your spending within 30% of your credit limit and pay on time. This will show the credit bureaus that you are financially responsible.

Know more about the best business credit cards available on the market and buy a credit card that suits your business needs.

8- Pay Business Bills on Time

This is the basis of your business credit score. If you always pay your bills on time, you are bound to get a higher business credit score with time.

How does this affect your business credit score? Credit reports use the term ‘Days Beyond Term’. It counts the days after the due date you made the bill payment.

For example, you made a deal with your vendor at net-30 terms and you made payment after 32 days. Even a delay of only 1 or 2 days will affect your business credit score badly.

9- Monitor your Business Credit Report

Keep checking your business credit report. You’ll spot any errors, missing tradelines or credits, or any inaccuracies and you can correct them in time.

In case of an error, you can contact the business credit reporting agency, file a dispute and ask them to rectify the records.

If you are building your business credit, checking your business credit reports regularly is a must to sustain and increase growth.

Want to write a business plan?

Hire our best business plan writers now!

FAQs:

You can start a business credit score in 8 easy steps.

- Select the right business formation type

- Get Employer Identification Number

- Open a business bank account

- Add Trade References

- Establish Credit with Vendors/Suppliers who Report to Credit Reporting Agencies

- Get a business credit card

- Pay business bills on time

- Monitor business credit report regularly

Businesses also receive a credit score as individuals. A business credit score is used to check the creditworthiness of your business, see when you pay bills and how much credit can be extended to you.

You can check your business credit score for free in the following three ways:

- Dun & Bradstreet CreditSignal

- Request a Free Report at AnnualCreditReports

You are entitled to get one free business credit report every 12 months. Visit https://www.annualcreditreport.com/ and request your free business credit report and your business credit score.

You can check your business credit score with Experian, Equifax, and Dun & Bradstreet.

Dun & Bradstreet offers free business credit scores but Experian and Equifax will charge a fee for business credit reports.

Equifax gives business credit scores in the range of 1-100 where a higher score is better.

Equifax determines your business credit score on your business payment history. If you pay your business bills on time, your Equifax business credit score will be higher.

You can improve your business credit score in the 7 easy steps.

- Check your Business Credit Report Regularly

- Pay Bills on Time

- Keep Credit Utilization Ration Low

- Establish Credit with Suppliers & Vendors

- Increase the Number of Good Payment Experiences to Business Credit Report

- Spot and Dispute any Errors, Missing Credit, or Inaccuracies

- Minimize your Outstanding Balances

You’ll need a good business credit score for securing a business loan and funding.

Dun & Bradstreet measures business credit score on a scale of 1-100 where a higher score represents high creditworthiness for your business.

These 7 business credit cards don’t report to Personal Credit.

- Wells Fargo Business Platinum

- PNC Cash Rewards® Visa Signature® Business Credit Card

- U.S. Bank Business Platinum Card

- Costco Anywhere Visa® Business Card by Citi

- U.S. Bank Business Triple Cash Rewards World Elite Mastercard®

- Wells Fargo Business Secured

- CitiBusiness® / AAdvantage® Platinum Select® Mastercard®

American Express reports your financial activities to Dun & Bradstreet and Small Business Financial Exchange (SBFE) once a month.

Amazon reports business expenses to Dun & Bradstreet and Small Business Financial Exchange (SBFE).

Capital One reports your credit card activities to business credit bureaus. It reports your credit activity as a small business credit card.

If you miss any payments or increase your credit utilization ratio, it will negatively affect your personal credit score.

Yes, Chase Business Credit Card reports to Dun & Bradstreet and contributes to your business credit score.